Case Study: Diversifying Covered Calls by Expiration Dates

Use a 30/60/90-day covered-call ladder to smooth income, cut assignment risk, and boost premium income in a six-month case study.

Investors often rely on selling covered calls with a single expiration date, typically 30-45 days out. While straightforward, this approach exposes the entire portfolio to concentrated risks on one date. A diversified expiration strategy, known as laddering, spreads call expirations across multiple timeframes (e.g., 30, 60, and 90 days). This improves covered call risk management, smooths income, and minimizes volatility.

Key Takeaways:

- Single Expiration Risks: All positions face assignment risk simultaneously, leading to higher volatility and management complexity.

- Laddering Benefits: Staggered expirations reduce drawdowns, lower assignment frequency, and provide more consistent cash flow. This approach is often compared to covered calls vs cash-secured puts to determine the best income strategy.

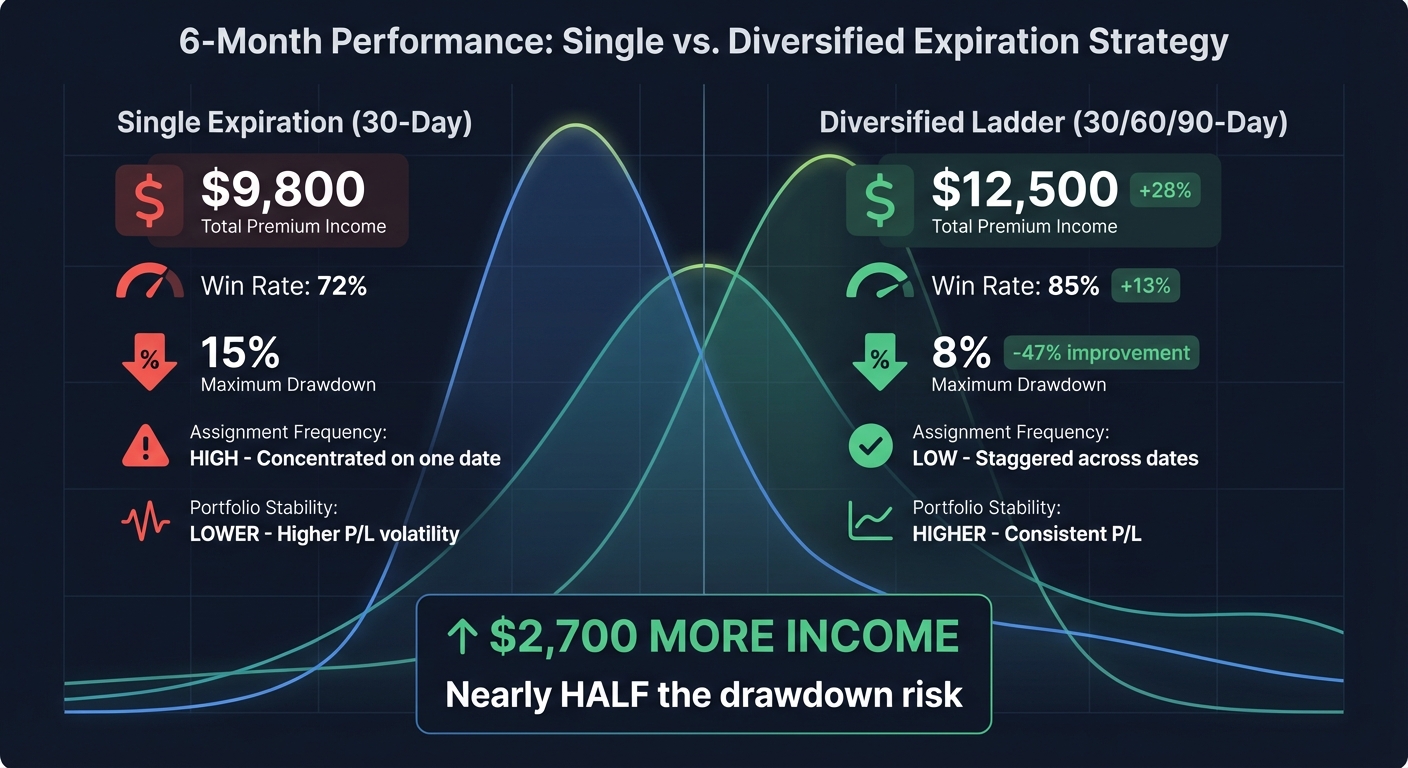

- 6-Month Results: A laddered portfolio earned 28% more premium income ($12,500 vs. $9,800), had an 85% win rate (vs. 72%), and saw lower drawdowns (8% vs. 15%).

Starting Point: Single Expiration Covered Calls

Portfolio Setup

The portfolio, valued at $100,000, was divided among 400 AAPL shares (purchased at $250 each), 300 MSFT shares (at $333.33 each), and 1,000 XYZ shares (at $100 each). On the first trading day of each month, 30-day out-of-the-money (OTM) covered calls were sold for all holdings, targeting a delta of 0.30 (indicating roughly a 30% chance of assignment).

This strategy generated monthly premiums ranging from 1% to 2.5% of the portfolio's value. Over the 30-day cycle, theta decay - the rate at which options lose value as expiration nears - accelerated. It started at approximately $0.12 per day at 30 days-to-expiration (DTE) and increased to over $0.30 per day by the final week. In a sideways market, where stock prices fluctuated within a narrow range, this time decay worked to the portfolio's advantage, allowing most options to expire worthless.

The next step was to evaluate how this setup performed over six months in a sideways market.

6-Month Performance in a Sideways Market

The strategy was designed to take advantage of rapid theta decay while keeping assignment risk under control. Over six 30-day cycles, the portfolio earned $11,400 in total premiums, averaging $1,900 per month. However, there were two instances of assignment: AAPL in month three and MSFT in month five. Both occurred on expiration Fridays when the stocks closed slightly above their strike prices, triggering automatic exercise.

One notable challenge came during month four, when a sudden tech rally drove all positions close to their strike prices within a 72-hour window. This situation underscored a significant vulnerability: the portfolio's exposure to the same market forces across all positions at the same time. While the rally subsided before expiration, it highlighted the risk of simultaneous assignment in a concentrated portfolio.

Additionally, the final week of each cycle brought heightened gamma risk - a scenario where small price movements caused outsized changes in option values. This amplified sensitivity made managing positions more complex as expiration approached.

sbb-itb-a9ac3c2

Diversified Expiration Strategy: How It Works

Setting Up the Expiration Ladder

Switching to a diversified expiration strategy spreads risk across different time horizons by dividing shares among 30-, 60-, and 90-day expirations. For example, if you own 300 shares, you might allocate 100 shares to each expiration tier. This approach ensures your portfolio is exposed to multiple expiration dates simultaneously, providing a balanced structure that you can map out using an options strategy planner. Shorter-term calls benefit from faster theta decay and offer higher annualized income, while longer-term calls provide larger total premiums and reduce the likelihood of frequent assignments. This setup creates a solid foundation for managing both risk and option decay.

Benefits of Staggered Expirations

The main advantage of this strategy is spreading out risk. Instead of facing the possibility of all positions being assigned on a single expiration date, only a portion of your portfolio is at risk at any given time. This directly addresses the concentrated risk associated with single-expiration strategies. Additionally, staggering expirations smooths out theta decay across your portfolio. While shorter-term options decay faster, mid- and longer-term positions offer steadier decay, creating a more balanced cash flow. This approach avoids the "feast-or-famine" cycle often seen with single monthly expirations, leading to reduced daily profit and loss volatility and more consistent income.

Comparison Table: Single vs. Multiple Expirations

The table below highlights the differences between single-expiration strategies and a diversified expiration ladder:

| Metric | Single Expiration (30-Day) | Diversified Ladder (30/60/90-Day) |

|---|---|---|

| Annualized Income | Higher yield potential | Moderate; blended across cycles |

| Assignment Risk | All shares at risk on one date | Only one-third of shares at risk per cycle |

| Daily P/L Volatility | Higher sensitivity to market moves | Lower daily fluctuations |

| Gamma Risk | High in final week | Diversified; only one leg in high-gamma zone |

| Management Effort | High; requires monthly monitoring | Moderate; staggered roll dates |

While a diversified expiration ladder might slightly reduce annualized returns, it provides more stability and flexibility. Instead of dealing with the stress of managing all positions during a single expiration week, this strategy spreads decisions across the calendar, offering a smoother and more predictable experience.

6-Month Results: Performance Comparison

Single vs Diversified Covered Call Strategy: 6-Month Performance Comparison

Income and Risk Numbers

The diversified strategy outperformed its single-expiration counterpart, delivering 28% more premium income, a higher win rate, and significantly reduced drawdowns. Over the six-month period, the laddered approach brought in $12,500 in total premium income, compared to $9,800 from the single-expiration strategy - a difference of $2,700. This approach also increased the win rate from 72% to 85%, meaning fewer positions ended up losing money or needing adjustments.

Risk management saw a major improvement as well. The maximum drawdown for the diversified strategy was just 8%, compared to 15% for the single-expiration approach - nearly double the loss during periods of volatility. This aligns with findings that covered call strategies tend to reduce portfolio volatility by 30–40%. By spreading positions across 30-, 60-, and 90-day expirations, the portfolio handled market swings more effectively, all while maintaining growth potential.

Assignment Frequency and Portfolio Stability

By staggering expirations, only one-third of the shares were exposed at any given time. This helped avoid concentrated assignment pressure during volatile periods and allowed for proactive rolling at 21 days to expiration. For example, when the market became turbulent mid-study, the single-expiration portfolio faced concentrated assignment pressure during a bullish week, forcing a full portfolio reset. In contrast, the laddered strategy enabled rolling individual positions, avoiding unnecessary assignments and maintaining better control.

"Laddering options expiration dates reduces risk and increases success." – Kai Zeng, Director of Research, tastylive

Instead of experiencing sharp swings tied to a single expiration cycle, the laddered approach provided steady cash flow throughout the six months. This consistency proved especially valuable during November's market rally, where the single-expiration portfolio struggled with unpredictable price movements in short-term contracts.

Results Table: Side-by-Side Metrics

Below is a comparison of key metrics for both strategies:

| Metric | Single Expiration (30-Day) | Diversified Ladder (30/60/90-Day) |

|---|---|---|

| Total Premium Income | $9,800 | $12,500 |

| Win Rate | 72% | 85% |

| Maximum Drawdown | 15% | 8% |

| Assignment Frequency | High (concentrated on one date) | Low (staggered across dates) |

| Portfolio Stability | Lower (higher P/L volatility) | Higher (consistent P/L) |

These results not only highlight the advantages of a diversified approach but also set the stage for discussing advanced risk management strategies in the next section.

Risk Management with ThetaEdge

Building on the improved performance of the diversified ladder, this section focuses on advanced strategies to manage risks effectively.

Building on the improved performance of the diversified ladder, this section focuses on advanced strategies to manage risks effectively.

Lowering Correlation Risk

Spreading covered calls across various expiration dates helps reduce timing risk - the risk of entering all positions at once during periods of unfavorable volatility or pricing. A laddered approach staggers your positions, ensuring different contracts are at various lifecycle stages. While some benefit from steady time decay, others remain protected from short-term price movements.

Gamma risk becomes more pronounced in the final seven days before expiration. During this period, even small stock price changes can erase weeks of earned income. Rolling positions at 21 days to expiration (DTE) allows you to lock in 60–80% of the maximum profit while avoiding this high-risk window entirely. By staggering expirations, only a portion of your portfolio is exposed to heightened gamma risk at any given time, promoting overall stability.

"Theta is your friend; gamma is your enemy. Hold if profitable (theta wins). Close if losing (gamma risk explodes)." – DaysToExpiry

This staggered structure creates a steady income rhythm, where different parts of your portfolio are at various stages - some resolving, others mid-cycle, and new ones just beginning. This results in smoother daily profit and loss, fewer concentrated assignment events, and a more predictable cash flow pipeline. These strategies lay the foundation for leveraging tools designed to simplify managing a diversified expiration ladder.

Using ThetaEdge for Portfolio Management

Managing a laddered expiration strategy means tracking multiple positions across different timeframes — which contracts are approaching roll dates, what your aggregate Greek exposure looks like, and where the income is coming from. ThetaEdge is built for exactly this.

The Strategy Analyzer compares covered-call opportunities across 30-, 60-, and 90-day expirations side by side, with clear ROI and risk-adjusted metrics for each timeframe. The Roll Opportunities tool surfaces positions approaching 21 DTE and presents your roll options — extend time, adjust strike, or both — so you can evaluate the trade-offs and act on your terms.

Daily AI Reports flag expiring positions across your ladder so nothing slips through the cracks. Portfolio Greeks consolidate your Delta, Gamma, Theta, and Vega exposure into a single view, showing how market moves affect your entire strategy — not just individual trades. And with Thetix Chat, you can ask questions like "How much gamma risk do I have this week?" and get a clear answer without digging through spreadsheets.

"Running the hedge fund, I created institutional tools that could analyze thousands of scenarios in real-time... ThetaEdge empowers [investors] to do it with the same tools the elite have always used." – Maxim Khailo, Founder & CEO, ThetaEdge

Over 500 investors are already using these tools to manage their covered-call strategies. Free beta access is open if you want to test the workflow with your own portfolio.

Conclusion: What This Case Study Shows

What We Learned

After six months of analysis, one thing became clear: diversifying covered calls across multiple expirations delivers better risk-adjusted returns compared to sticking with a single expiration date. Staggering expirations helps reduce timing risk, spreads out assignments, and creates a smoother cash flow.

The sweet spot for these trades lies in the 30–45 day-to-expiration (DTE) range. Rolling positions at 21 DTE captured 60–80% of the potential profit while sidestepping the turbulence of the final week. A study of 1.7 million trade ideas revealed that contracts with more than 20 DTE aligned much closer to theoretical outcomes, while shorter-term contracts under 20 DTE were far less predictable.

Using a laddered expiration strategy also mitigates the risk of multiple contracts expiring at the same time. By staggering expirations, you ensure that your positions are spread across different stages - some benefiting from steady time decay, others shielded from short-term market swings, and new positions just beginning their cycle.

Next Steps for Investors

Putting these findings into practice is a straightforward process. Start by setting up a three-tier ladder with expirations at 30, 45, and 60 days. Monitor these positions and use time-based exits at 21 DTE to decide whether to roll, close, or let them expire based on market conditions. Avoid contracts with less than 7 DTE, as they carry heightened gamma risk, which can quickly eat into premiums.

For those looking to simplify this strategy, ThetaEdge offers tools designed to make managing staggered expirations easier. Its Strategy Analyzer helps identify opportunities across different time frames, while the Roll Opportunities tool pinpoints the best adjustments at 21 DTE. Daily AI Reports provide ongoing updates to ensure each position is optimized. Originally built for institutional traders, these tools are now available for individual investors, with free beta access providing a chance to test these strategies before committing real capital.

FAQs

How do I build a 30/60/90-day covered-call ladder with my shares?

To build a 30/60/90-day covered-call ladder, you sell call options on the same stock but with staggered expiration dates - roughly 30, 60, and 90 days out. This approach spreads out income generation over multiple timeframes while helping to balance risk.

Here’s how it works:

- Own sufficient shares: You’ll typically need 100 shares for each call option you plan to sell.

- Pick strike prices wisely: Out-of-the-money strikes are often preferred to allow for some stock price appreciation.

- Stay proactive: Keep an eye on your positions and make adjustments as expiration dates get closer.

This method provides a steady flow of premiums while giving you flexibility to react to market movements.

When should I roll a covered call to avoid late-stage gamma risk?

When managing a covered call, you might want to think about rolling the position under certain conditions. For example, if the delta climbs to around 0.55–0.65, it signals a growing chance that your shares could be called away. Another key indicator is when the time value falls below 10–15% of the option’s total price. At this point, the option offers less upside potential, which might make rolling the call a smart move to maintain control and flexibility in your strategy.

How do I pick strike prices and deltas for each ladder rung?

When building a covered call ladder, strike prices and deltas play a critical role in balancing income, risk, and potential upside.

- Strike Prices: Your choice should align with your income goals and how much risk you're willing to take. Strikes that are out-of-the-money can provide a mix of premium income and room for the stock to grow, while strikes closer to the current price offer higher premiums but increase the likelihood of your shares being called away.

- Delta: A Delta in the range of 10-15% (0.10-0.15) is often a sweet spot. It allows you to collect reasonable premiums without taking on excessive assignment risk.

These guidelines aren’t set in stone - adjust them to reflect your outlook on the market and your personal risk tolerance.