5 Position Sizing Tips for Balanced Portfolios

Five practical position-sizing rules to cap per-trade losses, adjust for volatility, limit concentration, scale entries, and rebalance.

Position sizing is the backbone of smart investing - it’s how you decide how much capital to allocate to each trade while managing risk. The goal? Protect your portfolio from devastating losses while maximizing returns. Here's what you need to know:

- Limit Risk Per Trade: Use the Fixed Percentage Risk Rule to cap losses at 1–2% of your total account.

- Account for Volatility: Adjust position sizes based on a stock’s volatility using tools like Average True Range (ATR).

- Set Limits: No single stock should exceed 10% of your portfolio, and no sector should go beyond 35%.

- Build Gradually: Scale into positions over time to reduce timing risks.

- Rebalance Regularly: As your portfolio grows or shrinks, rebalance to maintain consistent risk exposure.

These strategies help reduce drawdowns, stabilize returns, and keep your portfolio resilient during market swings.

Impact of Position Sizing on Portfolio Drawdowns and Recovery Requirements

1. Use the Fixed Percentage Risk Rule

The Fixed Percentage Risk Rule is simple: limit your risk on any single trade to 1–2% of your total account equity. This isn’t about how much you invest in a position - it’s about capping the potential loss if the trade goes against you. Understanding the difference between your total investment and the risk you’re willing to take is key.

Why Risk Management Matters

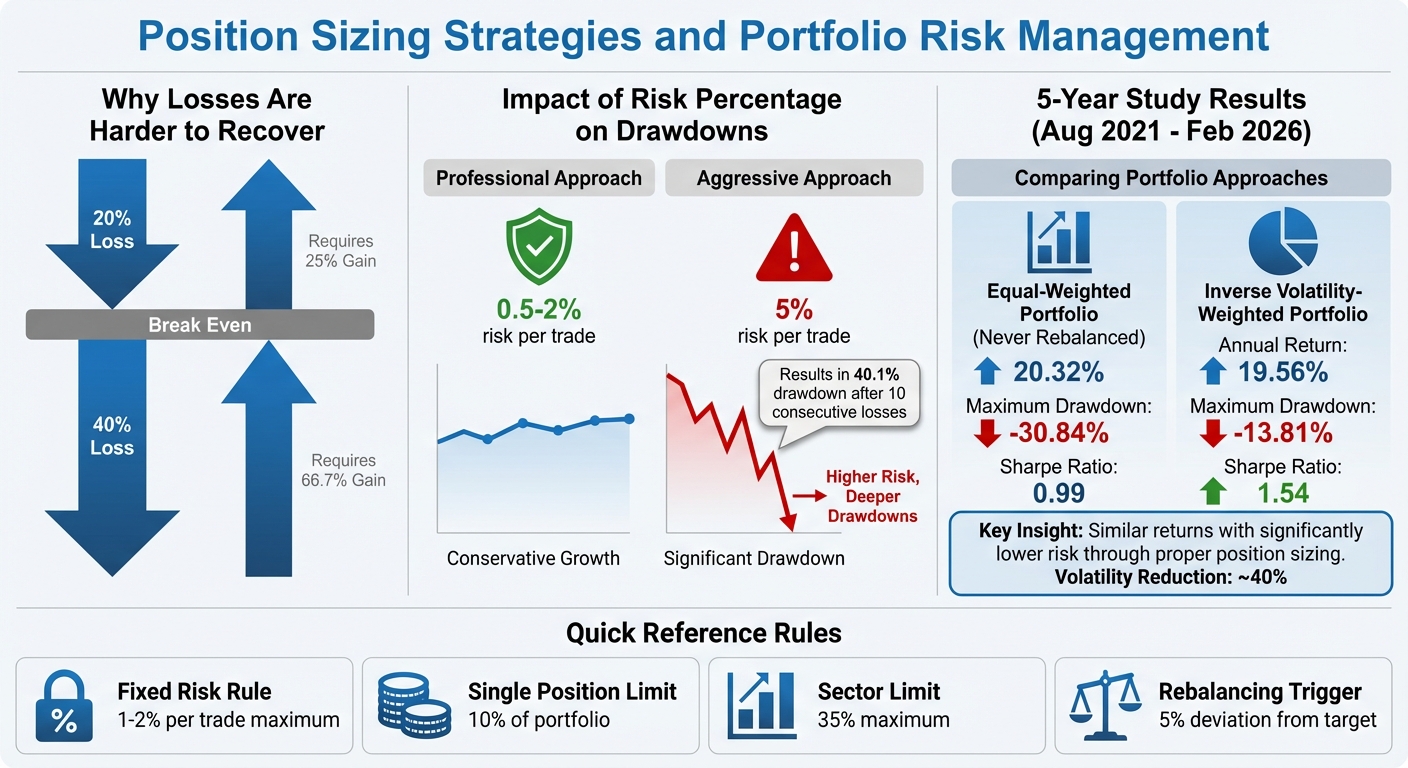

Losses are harder to recover than they seem. For example, a 40% loss requires a 66.7% gain just to break even. By capping each trade's risk at 1–2%, you create a buffer that protects your account from devastating drawdowns. Many professional traders stick to risking between 0.5% and 2% per trade. In contrast, risking 5% per trade could result in a 40.1% drawdown after only 10 consecutive losses.

Here’s a practical example: Back in February 2026, Sarah and Mike both entered a long Bitcoin position at $68,500 with a stop at $67,000. Sarah followed the 1% rule on her $10,000 account, risking just $100, while Mike used 10× leverage. When Bitcoin dipped to $66,800, Sarah’s position was manageable, but Mike got liquidated. Even though Bitcoin eventually hit $72,000 and Sarah made a $450 profit, Mike was already out of the game.

How to Apply It

The math is straightforward:

Shares = (Account Size × Risk % per trade) ÷ (Entry Price − Stop-Loss Price).

Let’s say you have a $50,000 account and follow the 1% rule, risking $500 per trade. If you’re buying a stock at $100 and set a stop-loss at $95, you’d buy 100 shares ($500 ÷ $5). Your maximum loss would be capped at $500.

Adjusting for Market Changes

This rule naturally adapts to changing conditions. For more volatile assets, you’ll need wider stop-losses, which means smaller position sizes to maintain the same dollar risk. During periods of high volatility, consider reducing your position sizes by 25–50% ahead of significant events to minimize gap risk. Additionally, recalculating your risk amount weekly as your account balance fluctuates ensures your risk percentage stays consistent. This disciplined approach helps you stay flexible while protecting your portfolio over time.

sbb-itb-a9ac3c2

2. Adjust Position Size Based on Volatility and Confidence

Not all stocks carry the same level of risk. A $5,000 investment in a steady utility stock is a completely different story from putting the same amount into a volatile biotech company. That’s where volatility-aware sizing comes into play - it helps you keep risk consistent across your portfolio.

A useful tool here is the ATR (Average True Range) method: Position Size = Account Risk ÷ (ATR × Multiple). For example, if you have a $100,000 account and are willing to risk 1% ($1,000) per trade, here's how it works: if a stock’s ATR is $1.00, you’d buy 500 shares. On the other hand, if another stock’s ATR is $5.00, you’d only purchase 100 shares to maintain that same $1,000 risk level. This approach ensures your position size adjusts to the stock’s volatility.

Why This Approach Works

Using ATR-based sizing doesn’t just stabilize risk - it can also improve overall performance. Studies show this method can reduce drawdowns by 25% during volatile periods compared to fixed-percentage sizing. The idea is simple: when volatility increases, your position size decreases, which helps protect your account from outsized losses. To further safeguard your trades, set your stop-loss at 1.5×–3× ATR. This buffer helps you avoid being shaken out by short-term price swings.

Adjusting for Market and Portfolio Changes

Flexibility is key. When volatility is low, you might risk 1–2% per trade. But when the VIX spikes, scaling back to 0.5–1% can help manage risk. Similarly, before major events like earnings announcements, consider halving your position size to account for the potential price gaps caused by event-driven volatility.

While volatility determines your base position size, confidence in your options strategy planner allows for further refinement.

"Position sizing and portfolio construction still do not get the attention they warrant." – Michael Mauboussin

Confidence adjustments can be based on historical success rates. For instance, if a bull flag pattern has a 67.9% success rate, you might apply a 1.2× multiplier to your base position size. However, even with maximum confidence, no single position should exceed 20–25% of your total account. To stay aligned with changing conditions, reassess volatility and price targets monthly.

3. Set Sector and Single-Position Limits

To manage risk effectively, avoid letting any single stock exceed 10% of your portfolio or any single sector surpass 35%. These limits act as safeguards, protecting your portfolio from heavy losses caused by a company’s failure or a sector-wide downturn. This approach not only reduces exposure but also strengthens diversification across your investments.

Risk Management Effectiveness

Capping risk per position is a cornerstone of sound investing. By sticking to the 10% and 35% limits, you reduce the chance of what traders call the "risk of ruin" - a scenario where one bad decision could cripple your portfolio. These boundaries ensure that even if you face multiple setbacks, your portfolio remains resilient over the long term.

"If it's determined that there's too much put on the line in one particular sector, then that can be an indication that the portfolio needs to be further diversified." – Harvey Sax, Alpha Wealth Funds

Impact on Portfolio Diversification

Diversification isn’t just about owning a variety of stocks - it’s about spreading your investments across assets that don’t move in unison. For example, holding 20 tech stocks isn’t helpful if they all react the same way to interest rate hikes. During market downturns, correlations between stocks often increase, meaning several positions could drop together. By capping sector exposure, you reduce this risk and avoid making an accidental concentrated bet.

Ease of Implementation for Self-Directed Investors

Setting these limits is simpler than it might seem. Use the S&P 500 sector weights as a guide - technology, for instance, usually makes up about 30% of the index, while healthcare represents around 13%. You can also follow the 75-5-10 rule: allocate 75% of your portfolio to a mix of securities, limit individual positions to 5%, and avoid holding more than 10% of any company’s voting stock. Most trading platforms offer tools to track your allocations and alert you when positions exceed your targets. By keeping individual and sector exposures in check, you maintain the disciplined approach to position sizing discussed earlier. This discipline is also essential when using advanced techniques like a covered call strategy to generate income from existing holdings.

4. Build Positions Gradually Over Time

Instead of diving in with your full investment amount right away, consider scaling into positions over time. This approach helps reduce the risk of making poorly timed entries and encourages a balanced risk profile across your portfolio. A practical method to start is the 50/50 rule: invest half of your planned amount initially, and only allocate the remaining half once the position moves in your favor by at least 0.5 times your initial risk. This method allows for better adaptability in volatile markets and smoother execution.

Risk Management Effectiveness

Taking a gradual approach can shield you from the consequences of a single bad decision. For example, if an investment drops 20%, it requires a 25% recovery to break even. A 40% drop, however, demands a 66.7% gain. To manage this, professional traders often limit their risk to just 0.5% to 2% per trade, which helps them endure losing streaks. Gradually building positions allows you to use market confirmation to your advantage, improving your risk/reward ratio and reducing the impact of sudden downturns.

Adapting to Market and Portfolio Changes

This strategy also provides flexibility during times of market uncertainty. For instance, if volatility spikes - measured by the Average True Range (ATR) exceeding 1.5 times its usual level - you might reduce new position sizes by 25–50% to account for increased gap risk. Alternatively, you can use an equity curve circuit breaker: if your account value drops below its 20-day moving average, cut new position sizes by 50% to avoid emotionally driven trades.

Additionally, research suggests that reviewing and updating your price targets and conviction levels monthly, rather than every six months, can triple your return on invested capital. This allows you to adjust position sizes based on current market data instead of outdated assumptions.

Simplicity for Self-Directed Investors

Implementing this strategy is straightforward. Treat each day as a new decision point - if you wouldn’t add to a position at today’s price, consider allocating that capital elsewhere. A simple spreadsheet can help you manage this process, with columns for account balance, risk percentage, entry price, stop loss, and current ATR. This removes the guesswork and avoids emotional decision-making. For correlated trades, such as multiple tech stocks, treat them as a single group and cap total risk at 1% to prevent overexposure.

Self-directed investors can also leverage tools like ThetaEdge, which provide real-time insights and support for disciplined, incremental position scaling. This method not only simplifies execution but also aligns with sound risk management practices.

5. Rebalance as Your Account Grows or Shrinks

Risk Management Effectiveness

When your portfolio grows or shrinks, sticking to the same position sizes can unintentionally alter your risk exposure. This becomes particularly important if you've been using fixed risk and volatility adjustments. Without rebalancing, assets that perform well will naturally take up a larger share of your portfolio, potentially increasing your overall risk beyond your original plan. For instance, imagine tech stocks outperform and grow from 30% to 50% of your holdings - this could dramatically increase your portfolio's volatility.

A study covering August 2021 to February 2026 highlights this issue. Louis Llanes, CFA, compared two portfolios containing Robinhood (HOOD), VanEck Merk Gold Trust (OUNZ), Hershey (HSY), and the iShares Core S&P 500 ETF (IVV). One portfolio was equal-weighted (25% each, never rebalanced), delivering a 20.32% annual return but suffering a –30.84% maximum drawdown. Meanwhile, the other portfolio used an inverse volatility-weighting strategy, adjusting positions based on 12-month rolling volatility. It achieved almost the same annual return (19.56%) but with a significantly lower drawdown of –13.81%.

"How you size positions and manage risk is just as important as what you buy."

– Louis Llanes, CFA, CMT

This underscores the importance of rebalancing as a tool for maintaining a consistent risk profile.

Ease of Implementation for Self-Directed Investors

Rebalancing is a practical way for individual investors to keep their portfolios aligned with their strategies. A simple trigger for rebalancing could be when any asset class deviates by 5% or more from its target allocation. Alternatively, you can use a calendar-based approach, reviewing and adjusting your portfolio quarterly or annually to avoid reacting to daily market noise.

For taxable accounts, reinvest dividends or new contributions into underweighted positions to restore balance without selling assets and triggering capital gains taxes. If you need to withdraw cash, consider selling from assets that are overrepresented - this allows you to meet your cash needs while rebalancing at the same time. In tax-advantaged accounts like 401(k)s or IRAs, rebalancing becomes even simpler since you don't have to worry about tax consequences.

Adjusting to Changing Market or Portfolio Conditions

As your account value fluctuates, your position sizes should be recalibrated to maintain balance. Professional traders often manage this by risking a fixed percentage of their account rather than a fixed dollar amount, which helps them weather losing streaks regardless of market conditions. Regular rebalancing ensures that your portfolio stays aligned with your goals, keeping earlier strategies effective even as your account size or the market environment evolves.

Conclusion

These five position sizing strategies transform a collection of individual trades into a well-rounded risk management framework. The fixed percentage rule ensures no single loss can jeopardize your portfolio. Adjusting for volatility prevents positions in highly volatile stocks from dominating your risk. Sector limits guard against unintended overexposure to correlated trades, and gradually building positions allows flexibility as new information comes to light.

The results can be striking. In Louis Llanes' five-year study, concluding in February 2026, shifting from equal weighting to inverse volatility weighting - applying these principles - reduced portfolio volatility by around 40%. It also lowered maximum drawdowns from -30.84% to -13.81%, all while maintaining nearly the same returns. This approach led to a Sharpe ratio of 1.54, significantly outperforming the 0.99 achieved by the equal-weighted portfolio. The takeaway? A risk-conscious strategy can help you stay composed during market swings, avoiding rash decisions.

"Security selection provides the fuel. Risk management keeps the engine from overheating under stress."

– Louis Llanes, CFA, CMT

Adopting a structured approach to position sizing can improve returns by as much as four percentage points, while strengthening your resolve during challenging market conditions. The true advantage isn't just better performance - it's the ability to stick with your strategy. When your portfolio is sized appropriately, drawdowns become manageable, reducing the temptation to abandon your plan during tough periods.

For investors managing multiple positions, tools like ThetaEdge can simplify the process. This platform connects to over 80 brokerages via read-only access, offering insights into your portfolio's risk exposure and highlighting opportunities that align with your sizing rules. By providing professional-grade analysis without executing trades, ThetaEdge helps you maintain discipline and stay in control of your investment strategy.

FAQs

How do I pick the right stop-loss for position sizing?

To determine the right stop-loss, start by deciding what percentage of your capital you're comfortable risking on a single trade - commonly around 1-2%. For example, if you have a $25,000 account and choose to risk 1%, that equates to $250. Next, calculate the difference between your entry price and your intended stop-loss price. Divide your risk amount ($250) by this difference to figure out how many shares to trade. This approach ensures your stop-loss protects your portfolio from excessive losses while staying within your risk tolerance.

What should I do when my holdings are highly correlated?

If your investments are closely tied in performance, it's crucial to address concentration risk. One way to do this is by diversifying and adjusting the size of your positions. Running correlation stress tests can help you see how your assets move in relation to each other, allowing you to identify and reduce positions that are too closely connected.

Another helpful strategy is setting portfolio heat limits, such as capping risk exposure to 3-5% per position. This prevents your portfolio from becoming overly dependent on correlated assets. Regularly reviewing your portfolio's overall risk exposure ensures it stays balanced and aligned with your goals.

How often should I rebalance in a taxable account?

Rebalancing a taxable account is typically suggested every 6 to 12 months or whenever your asset allocation strays significantly from your set targets. This approach helps you keep your risk level in check while also factoring in tax consequences and transaction fees.