How Time Decay Impacts Covered Calls Near Expiration

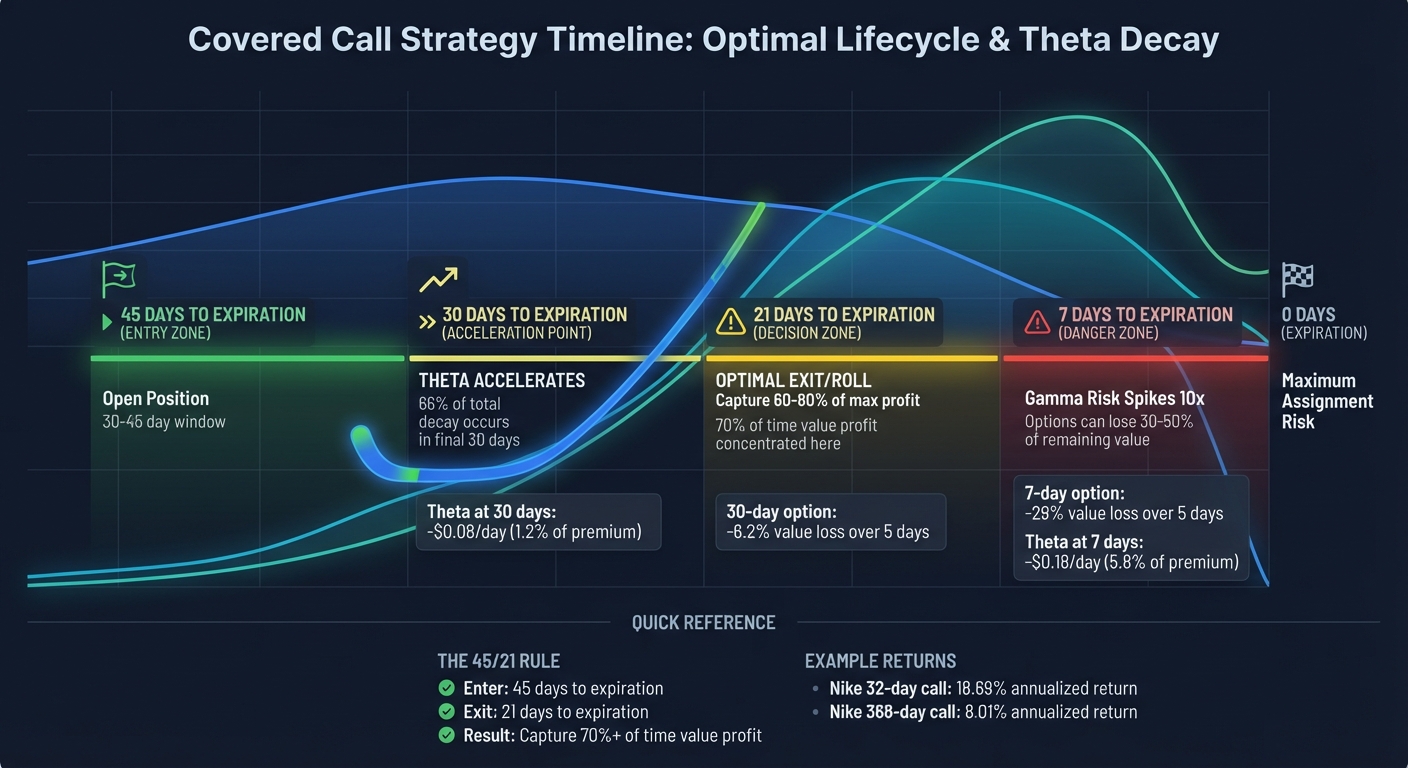

Use theta to generate income with covered calls: target 30–45 days to expiration, and close or roll around 21 days to limit assignment risk.

When selling covered calls, time decay - or theta - is your ally. Options lose value as expiration nears, with decay accelerating in the final 30 days. This creates income opportunities but also increases covered call risks. The key is timing: aim for 30–45 days to expiration, where theta decay is meaningful but risks remain manageable. Close or roll positions around 21 days to lock in profits and avoid last-minute volatility.

Key points:

- Theta Decay: Most rapid in the last 30 days, especially for at-the-money options.

- Income vs. Risk: Selling covered calls generates income but caps upside and risks assignment.

- Optimal Timing: Open positions 30–45 days out; close or roll around 21 days to avoid heightened gamma risk.

- Adjustment Strategies: Roll positions to extend income opportunities or protect shares.

Tools like ThetaEdge can simplify tracking theta decay, assignment probabilities, and rolling decisions, helping you make the most of covered call strategies.

Covered Call Strategy Timeline: Optimal Entry and Exit Points for Maximizing Theta Decay

How Time Decay (Theta) Works in Options

What Is Time Decay (Theta)?

Theta represents how much an option's price decreases each day due to the passage of time, expressed in dollar terms. For instance, if an option has a theta of -0.05, it loses about $0.05 per share daily, translating to approximately $5 per standard 100-share contract. This decline happens continuously, so holding an option through a weekend results in around three days' worth of decay.

It's important to note that theta only impacts the extrinsic value of an option - the portion of the premium tied to time and uncertainty. As expiration approaches, the chance of the option ending profitably diminishes, causing this extrinsic value to shrink. The intrinsic value, if any, remains unaffected.

For those selling covered calls, this daily erosion is advantageous because they effectively collect the time decay as income. As Ryan O'Connell, CFA, FRM, explains:

"Theta is the cost of owning optionality and gamma exposure."

Understanding why this decay accelerates as expiration nears is key to using an options strategy planner to manage theta strategically.

Why Theta Accelerates Near Expiration

For covered call sellers, the rapid increase in theta decay near expiration can amplify both income opportunities and potential risks.

Theta decay doesn't occur at a consistent rate. Instead, it follows a "hockey stick" pattern: slow and steady when expiration is far away, but sharply accelerating in the final 30 days. For at-the-money options, about 66% of the total time decay happens during this critical period.

Consider an analysis from February 2026 involving Apple (AAPL) stock priced at $195. Two at-the-money call options were compared:

- A 30-day option lost 6.2% of its value over five flat trading days, equating to -$0.08 per day (or 1.2% of the premium).

- A 7-day option, however, lost 29% of its value in the same period, averaging -$0.18 per day (or 5.8% of the premium).

This steep decline is most pronounced in at-the-money options, which are composed entirely of extrinsic value. In the final week before expiration, short-term options can lose as much as 30% to 50% of their remaining value.

Many experienced traders focus on a 30–45 day window, often referred to as the "Goldilocks zone." This period offers a balance: theta decay is substantial enough to generate meaningful income, yet it avoids the heightened volatility and assignment risks that come with the last few days before expiration.

sbb-itb-a9ac3c2

Covered Calls: Premium Income vs. Assignment Risk

Building on the concept of how theta accelerates as expiration nears, it's important to balance the allure of premium income with the potential risk of assignment.

How Covered Calls Generate Income

Covered calls let you sell the right for someone else to buy your shares at a specific price (the strike price) before a set expiration date. In return, you earn a premium, which is credited to your account. This premium has two components: intrinsic value and extrinsic value. The latter, tied to time, gradually fades as expiration approaches.

This time decay, or erosion of extrinsic value, works to the seller's advantage. As the expiration date gets closer, the chances of the option expiring worthless grow, turning that decaying value into profit. John Clarke from Strike Price explains it well:

"For option sellers, it's a reliable tailwind pushing your trade forward."

But there’s a catch. If the stock price rises above your strike price, you’re obligated to sell your shares at that level, limiting your potential upside. So, while premium income can be tempting, it’s essential to weigh it against the increasing risk of assignment as expiration nears.

Managing Assignment Risk Near Expiration

As expiration approaches, the risk of assignment ramps up significantly, especially in the final days. Early in the contract - say, with about 30 days remaining - a small move above the strike price might not lead to assignment because the option still retains extrinsic value. But with just a day or two left, even minor price moves can result in your shares being called away.

This risk is magnified by gamma, which measures how sensitive an option’s price is to stock movements. During the final week, even small stock price changes can cause big swings in option prices, making assignment harder to predict.

To navigate this risk, many traders adopt dynamic exit strategies. For instance, professionals often close or roll their positions around the 21-day mark - once they’ve captured 60–80% of the potential profit. Alternatively, they may close at 50% profit if there’s still plenty of time left, steering clear of the unpredictable final week.

If the stock starts nearing your strike price and you want to keep your shares, rolling the position is a common strategy. This means buying back the current call and simultaneously selling a new one, either with a later expiration or a higher strike price. Rolling not only protects your shares but also extends your opportunity to generate income.

Best Expiration Dates for Covered Calls

Understanding the timing for covered call expiration dates is crucial. The interplay of theta decay, assignment risk, and market volatility directly impacts the effectiveness of your strategy.

Why 30–45 Days Works Best

The sweet spot for covered call sellers often falls in the 30–45 day range. During this period, theta decay - how options lose value over time - accelerates meaningfully, offering a good balance between income potential and risk. By contrast, the final week before expiration tends to bring heightened volatility and gamma risk, which can make positions more sensitive to price swings.

For example, an option with 30 days left may lose about 1/30th of its value daily, while one with just 3 days remaining could lose up to 1/3rd of its value in a single day. While this rapid decay might seem appealing, the accompanying gamma risk often outweighs the benefits.

Consider a real-world scenario with Nike (NKE) stock: a 32-day call option generated an 18.69% annualized return, compared to just 8.01% from a 368-day call option. Many traders follow a "45/21 rule" - opening positions around 45 days to expiration and closing or rolling them at roughly 21 days. This approach captures over 70% of the option’s time value profit, which tends to concentrate in the final three weeks of the cycle.

This timing not only maximizes premium income but also provides a structured exit strategy, allowing for smoother adjustments.

Adjusting Positions as Expiration Approaches

As expiration nears and theta decay speeds up, it’s wise to lock in gains. Around 21 days to expiration, if you’ve captured between 50% and 75% of the maximum profit, it may be time to adjust your position. Closing or rolling the call at this stage helps secure profits while sidestepping the increased gamma risk of the final week.

"Income traders don't wait for 100% of the profit. They take 70% quickly, then repeat the cycle. Over a year, capturing 70% six times beats getting stuck holding a position that turns against you."

- Days to Expiry Trading Team

To roll your position, buy back the current call and sell a new one with a later expiration or higher strike price. Ideally, execute this roll for a net credit. Adjusting positions 7–10 days before expiration ensures tighter bid-ask spreads and minimizes slippage, while waiting until the last 1–2 days can erode profitability.

However, avoid rolling indefinitely in a losing position. If the stock price exceeds your strike by more than 5%, it’s usually better to close the position and reallocate your capital elsewhere. This disciplined approach helps maintain long-term profitability.

Using Professional Tools for Covered Call Analysis

Navigating the complexities of time decay and assignment risk requires more than just intuition. As expiration approaches, the effects of accelerating theta decay and rising gamma risk create a tight window for making the best decisions. Professional tools can simplify this process, eliminating the need for manual tracking and providing the data-driven insights you need.

ThetaEdge: Tools for Smarter Covered Call Decisions

ThetaEdge brings institutional-level analysis to individual investors. By securely integrating with over 80 brokerages through read-only access, it creates a unified dashboard tailored to your portfolio. This dashboard highlights covered-call opportunities specifically aligned with the stocks you already own.

Each opportunity card provides essential metrics, including risk profiles, profit potential, and assignment probabilities - key details as expiration nears. Additionally, ThetaEdge calculates your Portfolio Greeks (Delta, Gamma, Theta, and Vega) across all positions, giving you a clear view of how time decay and market movements affect your overall exposure.

"Running the hedge fund, I created institutional tools that could analyze thousands of scenarios in real-time... ThetaEdge empowers [self-directed investors] to do it with the same tools the elite have always used."

- Maxim Khailo, Founder & CEO, ThetaEdge

Beyond these features, ThetaEdge integrates AI-powered insights to streamline decision-making even further.

AI-Driven Insights for Managing Time Decay

Thetix, ThetaEdge's AI assistant, takes the complexity out of options analysis. It provides plain-language answers to questions about your portfolio, such as income potential or the risks tied to time decay on specific positions.

When positions approach the 21-day mark or begin to shift unfavorably, the Roll Opportunities tool steps in. It evaluates rolling scenarios with precise credit and debit calculations, ensuring you have clear options for action. To keep you ahead of the curve, ThetaEdge also delivers daily AI-generated reports straight to your inbox. These reports highlight expiring positions and recommended actions, helping you maximize theta gains during the 30–45 day sweet spot while steering clear of the heightened risks in the final week.

Conclusion

Time decay can be a powerful ally in covered call strategies when handled thoughtfully. The sweet spot lies in the "Goldilocks zone" - 30 to 45 days before expiration. This period strikes a balance: theta decay starts to accelerate, while gamma risk stays manageable. During this window, you can often capture around 60–80% of the maximum premium before the final week's volatility kicks in.

Interestingly, roughly 70% of an option's time decay profit occurs in the last three weeks. However, this is also when gamma risk can spike dramatically - up to 10 times higher than it was 30 days out. This sharp increase can quickly eat into any theta gains you've accumulated.

The solution? Close or roll positions before expiration. Many professional traders follow a 21-day rule, exiting or rolling at this point to lock in the majority of the premium while sidestepping the heightened risks of the final week. This approach aligns with the 21-day exit strategy mentioned earlier. As Andy Crowder from The Option Premium explains:

"Selling options isn't about predicting the next move. It's about structuring trades that profit if nothing happens, and letting time do the rest".

Managing the intricacies of time decay, assignment probabilities, and rolling decisions can feel overwhelming. Tools like ThetaEdge simplify this process. They help identify the best entry points, monitor positions, and flag those nearing the critical 21-day mark. By combining these strategies with advanced tools, you can enhance your returns while keeping risks in check.

FAQs

How does theta decay help covered call sellers?

Theta decay works in favor of covered call sellers by steadily eroding the value of the options they’ve sold. As the expiration date draws closer, this time decay accelerates, allowing sellers to keep a larger portion of the premium they initially collected. This can be especially beneficial when the underlying stock stays relatively stable or moves only slightly within the strike price range, as it maximizes the seller's potential profit from the trade.

What’s the risk of assignment near expiration?

As expiration approaches, the risk of assignment grows because of the sharp increase in time decay, also known as theta. This acceleration makes at-the-money options more likely to end up in the money, increasing the chances that your shares will be called away. Grasping how time decay affects options is key to navigating and managing covered call strategies with confidence.

When should I roll a covered call?

When a covered call nears expiration, especially if the stock price has climbed above the strike price, it might be time to consider rolling the position. Rolling allows you to avoid assignment and keep the trade going. The timing often hinges on factors like days to expiration (DTE). Many traders prefer rolling 30 to 45 days out to take advantage of time decay and maintain income potential.

Rolling can also be a smart move when market conditions shift, presenting opportunities for better premiums or improved risk management. It’s a flexible strategy that helps you adapt to changing circumstances while keeping your goals in focus.